Non-Banking Activities Services Offered by Banks

Non-Banking Activities

Non-Banking Activities

All banks perform non-banking activities along with their traditional functions.

A bank cannot survive without performing the following non-banking activities:

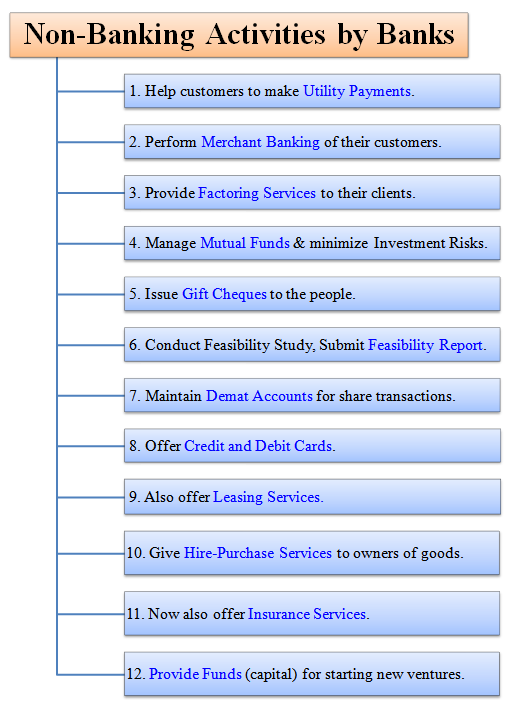

- Banks help their customers to make utility payments with ease.

- They perform merchant banking for their customers.

- They provide factoring services to their clients.

- They manage mutual funds and minimize investment risks.

- They issue gift cheques to the people.

- They conduct feasibility study and submit the feasibility report.

- They facilitate the share transactions by maintaining demat accounts.

- They offer credit and debit cards facility.

- They also offer leasing services.

- They give hire-purchase services to owners of various goods.

- They are now allowed to offer insurance services.

- They provide funds (capital) for starting new ventures.

Now let's discuss important non-banking activities performed by banks.

1. Utility Payments

Banks make utility payments for their customers. Utility payments include payment of an Electricity bill, Insurance premiums, phone bill, water bill, etc. They also pay SIP (Systmatic Investment Plan) payments to Mutual funds for their customers. These payments are made by using the Electronic Clearance Scheme (ECS). Banks charge a small (nominal) fee for making these payments.

2. Merchant Banking

Large banks perform merchant banking for their customers. They help them to raise finance. They give them advice about starting and running a business. They help their customers to make a profit in the stock exchange. They even do project management. They also help in expanding and modernizing the business of their clients. Today, banks help to revive (cure) sick industries. They also help in restructuring the business.

3. Factoring Services

Banks also provide factoring services to their clients. Factoring is an agreement between a bank (factor) and a business firm (client). Under this agreement, the business firm sells goods and services to their customers on credit. The bank (factor) purchases the customers' Bills Receivable or debtors account from the business firm. So, the business firm is guaranteed payment for their credit sales. However, the bank (factor) decides whom to give credit and how much credit to give.

4. Mutual Funds

Mutual funds are very popular because of expansion and diversification of the financial sector. The Unit Trust of India (UTI) was the first financial institution to start mutual funds in India. Many other banks now have mutual funds such as ICICI Mutual Fund, SBI Mutual Fund, HDFC Mutual Fund, etc. Mutual Funds are controlled by SEBI. Mutual Funds are purchased by investors because they offer minimum risk, maximum return and liquidity. Mutual funds with their resources and expertise invest on behalf of individual investors giving them capital appreciation with minimum risk. Mutual funds publish the NAV (Net Asset Value) of their funds daily. They also repurchase the units issued by them based on their NAV. Investors who like to play safe go for mutual funds.

5. Gift Cheques

Gift cheques are printed in attractive colours and designs. Gift cheques are issued by banks to the public. They can give these cheques as a present on auspicious occasions like marriage, birthdays, retirements, promotion, anniversary, etc. They are normally issued for Rs. 11, 21, 51 and 101. The purchaser makes full payment at the time of purchase. Gift cheques are transferable by hand delivery. These cheques have an expiry date. If a gift cheque is lost, a duplicate is issued. These cheques are payable on demand. The payee can claim the money at any branch of the issuing bank.

6. Feasibility Reports

Banks conduct feasibility study on behalf of the client and submit the feasibility report. This report shows chances of success of the project. Feasibility study is conducted before starting the project or business. Conducting feasibility study is not compulsory, but it gives many benefits to the businessman. Banks like IDBI or any commercial bank can conduct feasibility study in functional areas such as technical, managerial, financial and economic. After completion of feasibility study, the banks submit a feasibility report. Based on this report the businessman decides whether to do the project / business or not.

7. Demat Account

Demat is a commonly used name for dematerialization. Traditionally, shares were held in a physical form. Under dematerialization, shares are held in an electronic form. Demat account is like money kept in a savings account. You can deposit and withdraw the amount whenever you want. The transactions in electronic shares are quick, safe and simple. The shares purchased by a shareholder are transferred in his name on the next day of payout. A shareholder can sell and transfer his electronic shares from his office / house through a broker. Most of the shares are under demat. Banks facilitate the share transactions by maintaining demat accounts in their branch.

8. Credit and Debit Cards

Most large banks offer credit card facilities. Indian credit card market is growing at 30-35% per annum. ICICI, Citi, HDFC and SBI are the leading banks that offer credit card facilities. Most of the banks also offer debit cards to their customers. With the help of debit cards, the customers can make payments for the goods and services. This amount gets deducted from the balance they hold with the banks.

9. Leasing Services

Indian banks offer leasing services. In March 1994, RBI permitted banks to enter leasing finance provided following conditions are fulfilled:

- Specialized branches must be opened for doing this work.

- Banks may give lease finance up to 10% of their total advances.

- Assets in leasing will be treated as assets carrying 100% risk weightage.

10. Hire Purchase

Banks provide hire-purchase services. They finance hire-purchase contracts. Here, the owner of goods hires them to another party for a certain period and for the payment of a specific installment. The transfer of goods is passed on to the user after a definite period provided payment of all specified installments is clear.

11. Insurance

Banks are now allowed to offer insurance services through separate branches. Many Indian banks such as ICICI, IDBI, HDFC, etc., have entered into foreign collaborations to provide life insurance service in India. ICICI has joined Prudential Life, HDFC with Standard Life, IDBI with Fortis (now Federal) to provide life insurance services to Indians.

12. Venture Capital Services

Banks like ICICI, SBI, IDBI provides venture capital services. Here, banks provide funds for starting new ventures and for high-risk businesses with high-profit potential. Venture capital helps businessmen to get funds for highly risky projects. Venture capital means to buy shares in high-risk projects / businesses with high-profit potential.

No Comment Yet

Please Comment